How Much Does Paying Extra Per Month Move the Needle?

If you are stuck making minimum payments, even an extra $25 to $100 per month can move the needle. It can lower your balance faster, reduce interest, and help your credit utilization look better over time.

The fastest win is not a trick. It is simple math: less balance means less interest, and a lower balance compared with your credit limit can help your credit profile look stronger.

What does “move the needle” mean?

Paying extra “moves the needle” when it changes your balance enough to reduce interest, lower credit utilization, or shorten the payoff timeline.

It does not have to be a huge payment. A small payment you can repeat every month usually beats one large payment that leaves you broke and forces you to use the card again.

For credit cards, the two biggest signals are simple: pay on time and keep balances lower compared with your credit limits. FICO says payment history is 35% of a FICO Score, and amounts owed is 30%. That is why extra payments can matter when they reduce revolving balances and support steady repayment.

Lowers utilization

Your balance uses less of your available credit.

Speeds payoff

Less balance means fewer months stuck in debt.

Saves interest

More of your money goes to the balance, not the bank.

Builds momentum

A repeatable plan is easier to keep than a huge one-time push.

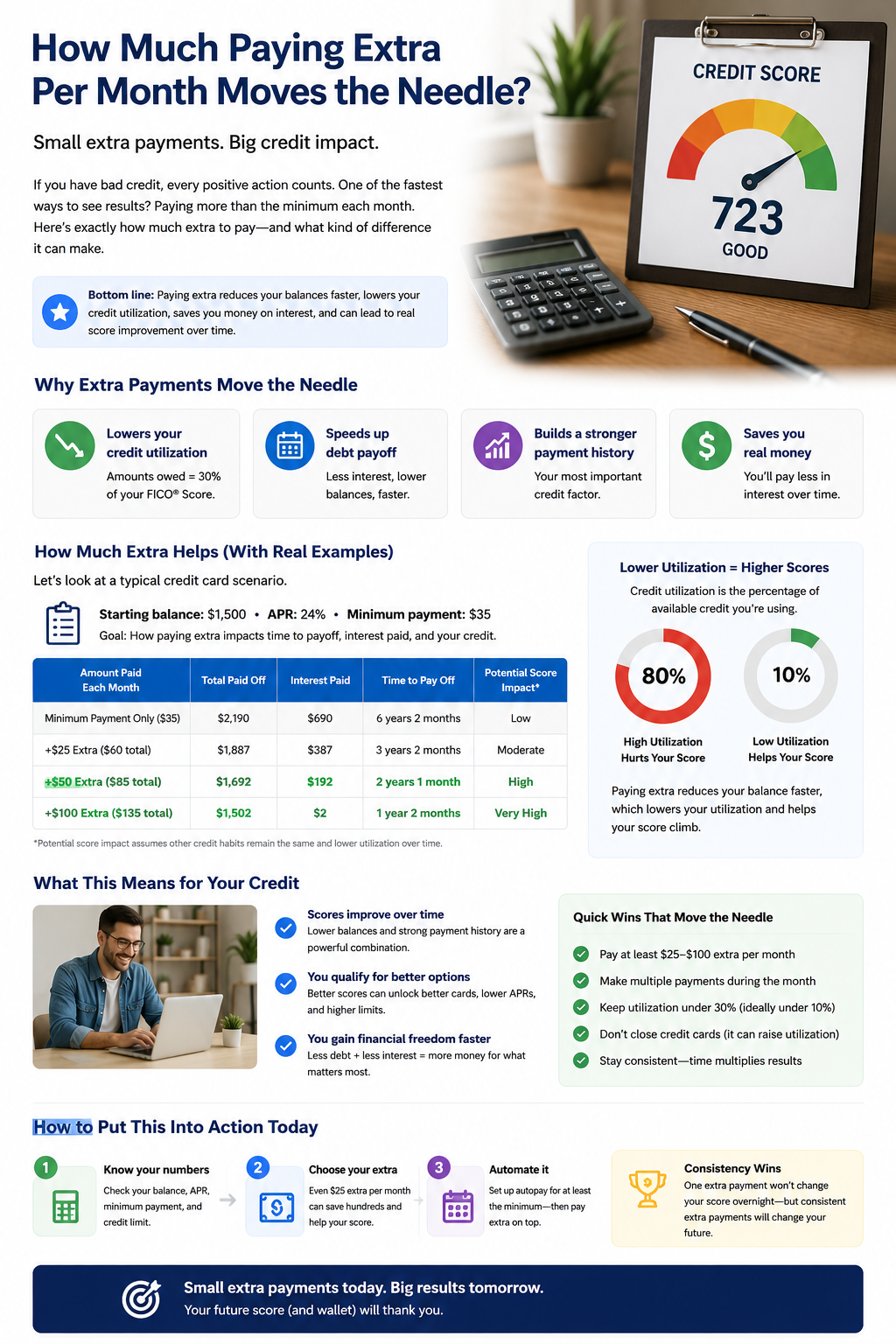

How much extra helps? A realistic example

On a $1,500 credit card balance at 24% APR, adding $50 extra per month could cut the payoff timeline from about 8 years to under 2 years if payments stay consistent.

This example uses a fixed payment so the direction is easy to see. Your real card minimum may change as your balance changes.

| Monthly payment | Total paid | Interest paid | Estimated time to pay off | What changes |

|---|---|---|---|---|

| Minimum only: $35 | $3,439 | $1,939 | About 8 years 3 months | Slow payoff, high interest drag |

| $25 extra: $60 total | $2,100 | $600 | About 3 years | Large interest savings |

| $50 extra: $85 total | $1,869 | $369 | About 1 year 10 months | Strong balance drop and faster utilization improvement |

| $100 extra: $135 total | $1,714 | $214 | About 1 year 1 month | Fastest payoff without needing a lump sum |

How extra payments affect utilization

Extra payments can help your credit profile when they lower your credit card utilization, which is your balance divided by your credit limit.

If your card has a $2,000 limit and a $1,500 balance, your utilization is 75%. That looks high. Getting that balance under $1,000 moves you below 50%. Getting it under $600 moves you below 30%.

Utilization levels on a $2,000 limit

What the chart really says

If your balance is high, your first goal is not perfection. Your first goal is to stop the balance from growing. Then aim for the next lower utilization zone: from 75% to under 50%, then under 30%, and later under 10% if possible.

How long does it take to cross key utilization levels?

The more you pay above the minimum, the faster you can move from high utilization into safer ranges.

Using the same $1,500 balance, 24% APR, and $2,000 credit limit, here is how long it may take to cross common utilization levels.

| Monthly payment | Under 50% utilization | Under 30% utilization | Under 10% utilization |

|---|---|---|---|

| $35 minimum only | About 56 months | About 78 months | About 93 months |

| $60 total | About 15 months | About 24 months | About 32 months |

| $85 total | About 9 months | About 15 months | About 20 months |

| $135 total | About 5 months | About 8 months | About 12 months |

Should you pay extra once or split payments during the month?

Splitting extra payments during the month can help if your issuer reports your balance before your due date.

A mid-cycle payment can reduce the balance that may be reported to the credit bureaus. A second payment by the due date keeps you current.

Pay at least the minimum before the due date

This protects payment history. Never sacrifice this step to make an extra payment somewhere else.

Add your extra payment as soon as income arrives

This lowers the balance sooner and reduces the chance that the money disappears into other spending.

Check the statement closing date

If you want a lower balance reported, try to pay before the statement closes, not only before the due date.

What most people get wrong

Most people think the extra payment has to be huge to matter. It does not.

The real problem is inconsistent action. Paying an extra $50 once helps a little. Paying an extra $50 every month changes the math.

- Wrong move: make one huge extra payment, then run the card back up.

- Better move: choose a smaller extra amount you can repeat.

- Best move: pay on time, pay extra, and stop adding new card debt while the balance falls.

How much extra should you pay?

The best extra payment is the largest amount you can repeat without missing rent, food, utilities, insurance, or minimum payments on other accounts.

If money is tight

Start with $25 extra. The goal is proof that you can repeat the habit.

If you have breathing room

Try $50 extra. This is the level where payoff timelines often start changing fast.

If you want aggressive progress

Use $100 extra or more, but only if it will not force new debt later.

When extra payments will not help much

Extra payments help less when new charges keep replacing the balance you just paid down.

That is the trap: you pay an extra $50, then put $75 of new spending on the card. The balance does not fall. Utilization does not improve. Interest keeps eating the progress.

How to put this into action today

You do not need a perfect plan. You need one clear number and one repeatable action.

Know your numbers

Write down your balance, APR, minimum payment, credit limit, due date, and statement closing date.

Choose your extra amount

Pick $25, $50, or $100. If you are unsure, start smaller and stay consistent.

Automate the minimum

This protects your payment history even if life gets busy.

Send the extra payment early

Pay extra when your paycheck arrives, not when the month is almost over.

Review every 30 days

Watch your balance, utilization, and interest charges. Adjust only if the payment still feels safe.

Small extra payments today. Better options tomorrow.

A small extra payment will not fix everything overnight. But it can start changing the numbers that keep you stuck: balance, interest, utilization, and time in debt.

If you can pay $25 extra, start there. If you can pay $50, that may move the needle faster. If you can pay $100 and still keep your budget safe, the timeline can change dramatically.

Common questions

Will paying extra raise my credit score?

It can help, especially if it lowers your credit utilization, but no score increase is guaranteed. Your full credit report, payment history, and timing of reported balances also matter.

Is it better to pay extra or pay the minimum?

Always pay at least the minimum by the due date. If you can safely pay extra on top of that, it can reduce interest and shorten the payoff timeline.

Is $25 extra per month enough to matter?

Yes, $25 extra can matter if you repeat it. In the example above, increasing the payment from $35 to $60 cut the payoff time from about 8 years to about 3 years.

Should I pay extra before the due date or statement date?

Pay the minimum before the due date. If you are trying to lower reported utilization, paying extra before the statement closing date may help because that is often the balance sent to credit bureaus.

Should I pay extra on one card or spread it around?

Keep every account current first. After that, many people focus extra money on the card with the highest interest rate or the highest utilization.

What if I cannot afford extra right now?

Do not force it. Protect essentials and minimum payments first. Then look for a small repeatable amount, even $10 or $15, when your budget allows.

Final takeaway

Paying extra moves the needle when it lowers your balance enough to reduce interest, cross utilization thresholds, and shorten your payoff timeline. Start with the extra amount you can repeat, protect your due dates, and let steady progress do the work.