Fee Trap Credit Cards: How to Spot Bad-Credit Card Fees Before You Apply

Updated May 2026 · 14 min read · Editorial review for bad-credit card shoppers

A fee trap credit card is a card that looks like a second chance but eats up your small credit limit with fees before it helps your credit. If you have bad credit, the safest move is to compare the total first-year cost, check whether the card reports to the credit bureaus, and avoid any offer that makes approval sound guaranteed.

Quick answer

What is a fee trap credit card?

A fee trap credit card is a card where the fees, terms, or approval claims are so costly or confusing that the card may hurt more than it helps. These cards often target people with bad credit, low scores, past denials, or no money for a security deposit.

The painful part is simple: you apply because you want a fresh start. Then the card shows up with a tiny limit, a big annual fee, a monthly maintenance fee, or an upfront program fee that eats your available credit before you buy anything.

That does not mean every bad-credit card is a scam. Some unsecured cards for bad credit are real tools. The question is whether the cost is clear, the card reports to the credit bureaus, and the card gives you a real path to something better later.

How fee trap credit cards work

Fee trap cards work by charging costs before the card gives you enough credit-building value. A card can be legal and still be a bad deal if too much of your limit goes to fees.

The card is marketed to people with bad credit, no deposit money, or past denials.

That is normal. When you are tired of rejection, approval feels like the win.

An annual fee, monthly fee, program fee, or high APR can make a small limit feel even smaller.

If there is no upgrade path, limit review, or clear credit-building value, the card becomes a costly holding pattern.

Who this guide is for

This guide is for people with bad or rebuilding credit who want a card without getting trapped by ugly fees. It is especially useful if you feel pressure to apply fast because you need approval.

You fear denial

You want a card that may fit your profile, but you do not want to waste another hard inquiry.

You fear fees

You have seen offers that look easy, but the annual fee, monthly fee, or setup fee feels wrong.

You want to rebuild

You want a tool that reports payments and helps you move to a better card later.

If any of that sounds familiar, you are not being paranoid. You are being careful. That is exactly how you should shop in the bad-credit card market.

Credit card fees to watch before you apply

The most dangerous fee is the one you ignore because approval feels more urgent. Before you apply, add the first-year cost and compare that number to the credit limit and credit-building value.

| Fee type | Why it matters | Visitor-first rule |

|---|---|---|

| Annual fee | Can reduce your real value before you use the card. | Ask whether the card gives enough credit-building value to justify it. |

| Monthly maintenance fee | Can quietly turn a “small” fee into a bigger yearly cost. | Add it to the annual fee before comparing cards. |

| Program or setup fee | May be charged just to open or access the account. | Be extra cautious if the fee comes before clear approval and terms. |

| Authorized user fee | Can cost extra if you add someone to the account. | Do not add users unless the benefit is clear. |

| Late payment fee | One late payment can hurt your credit and add cost. | Use autopay for at least the minimum payment. |

| Returned payment fee | You may be charged if your bank payment fails. | Pay from an account with enough funds. |

| Cash advance fee | Cash advances can trigger fees and interest fast. | Avoid cash advances unless it is a true emergency. |

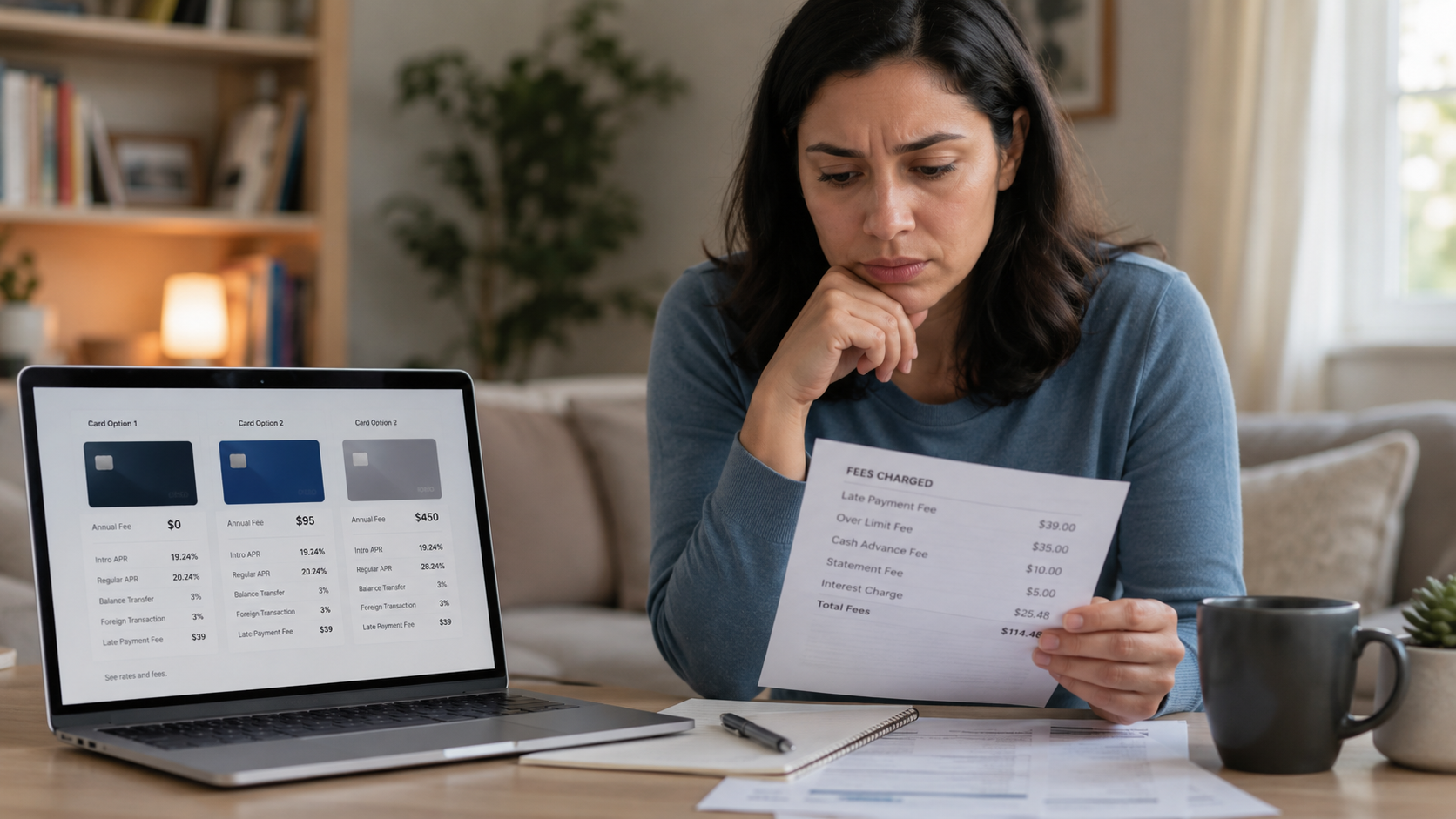

Visual: how a small fee stack changes the card

Bad-credit cards: fee-trap risk at a glance

The safest card is not always the easiest card to get; it is the one with costs you understand before applying. Use this table as a starting point, then verify current terms on the issuer’s site.

| Card | Why people consider it | Fee-trap risk to check | Best next question |

|---|---|---|---|

| Mission Lane Visa | Often considered for rebuilding and prequalification. | Check fee offer Terms may vary by offer. | Can I prequalify before a full application? |

| Avant Credit Card | Known as a simple unsecured option for fair or rebuilding credit. | Check annual fee Pricing can vary by offer. | Is the fee worth the credit-building value? |

| Credit One | Often appears in bad-credit searches and may offer unsecured cards. | Read fee box Fees and rewards can vary by product. | Is there a lower-fee alternative for my profile? |

| Indigo Mastercard | Often marketed to people rebuilding credit. | Watch total cost Review annual fee and available limit carefully. | How much usable credit remains after fees? |

| Milestone Mastercard | Often offers prequalification and bureau reporting language. | Watch terms Check APR, annual fee, and other costs. | Will this help enough to justify the cost? |

| Destiny Mastercard | Often appears as a no-deposit option for damaged credit. | Watch fee stack Read all pricing before applying. | Is a secured card cheaper for the same goal? |

This is not saying one card is automatically good or bad. It is saying the fee math matters before the application.

Approval reality: do not let fear rush you

Approval is never guaranteed, even when a card is marketed to people with bad credit. Issuers can look at your score, income, debt, credit history, recent inquiries, and current balances.

If you already got denied, do not panic-apply somewhere else the same night. Read the denial reason first. Fix what you can. Then choose the next card based on the reason, not emotion.

The 7-point Fee Trap Test

Before you apply, run the offer through this test. If two or more answers feel unclear, pause.

1. What is the first-year cost?

Add annual fees, monthly fees, setup fees, program fees, and any required upfront costs.

2. What is the usable limit?

Subtract fees from the starting limit. A small limit can become tiny fast.

3. Does it report to bureaus?

If it does not help build credit, it is harder to justify the cost.

4. Is approval language honest?

“Prequalified” is fine. “Guaranteed approval” should make you slow down.

5. Is the APR clear?

If you may carry a balance, a high APR can wipe out any benefit.

6. Is there an upgrade path?

A rebuilding card should be a bridge, not a long-term fee cage.

7. Is a secured card cheaper?

If the fees are higher than a deposit, secured may be the smarter rebuild path.

Fast rule

If you cannot explain the card’s cost in one sentence, do not apply yet.

Fee trap cards vs safer alternatives

A bad-credit unsecured card is better only when the cost is clear and the credit-building value is real. If the fee stack is ugly, a different path may be safer.

| Option | Best for | Strength | Weakness |

|---|---|---|---|

| Low-fee unsecured card | People who cannot or do not want to use a deposit. | No security deposit required. | Approval may be harder and fees can vary. |

| Secured credit card | People who want a clearer rebuild path and can afford a deposit. | Often lower fee risk. | Requires refundable deposit. |

| Wait and improve profile | People with recent denials, high balances, or too many inquiries. | Can improve approval odds later. | Does not solve an immediate card need. |

| Keep current card and upgrade later | People who already have a bad-credit card. | Protects account age while rebuilding. | Bad terms may still cost money. |

What most people get wrong

Most people compare bad-credit cards by approval chance, but they should compare by approval fit plus total cost. Approval feels good for one day. A bad fee setup can hurt for a year.

They chase “easy approval”

Easy can be expensive. A realistic card with fewer fees is usually better than a loud promise.

They ignore the first statement

Some fees can show up early. Always know what your first statement may look like.

They close too fast

If you already have a card, check the impact before closing. Credit age and utilization can matter.

Your next move

If you are worried about fee traps, do not apply until you can answer three simple questions: what will this cost in year one, will it report to the credit bureaus, and what better card could I move to later?

Common questions about fee trap credit cards

Are fee trap credit cards scams?

Not always. Some fee-heavy cards are legal products with real disclosures, but they may still be a poor value. A scam is different: it may promise approval for an upfront payment, hide who the lender is, or fail to provide a real card or clear terms.

What is the biggest warning sign?

The biggest warning sign is a promise of guaranteed approval paired with upfront or confusing fees. Legit lenders still review your application, identity, income, and credit profile.

Are no-deposit cards for bad credit always fee traps?

No. A no-deposit unsecured card can be legitimate. The risk is that some no-deposit cards charge enough fees to make the “no deposit” benefit less valuable.

Should I avoid every card with an annual fee?

No. An annual fee is not automatically bad. It becomes a problem when the fee is high compared with the credit limit, the card has weak benefits, or there is no clear credit-building value.

Is a secured card better than a high-fee unsecured card?

Often, yes. If you can afford the deposit, a secured card may offer a cleaner rebuild path with less long-term fee risk. But if you cannot afford a deposit, a carefully chosen unsecured card may still be worth comparing.

What should I do if I already have a high-fee card?

Do not panic-close it without checking the impact. Pay on time, keep the balance low, ask whether a lower-fee product or upgrade is available, and compare whether replacing it later makes sense.

Can a fee trap card still build credit?

It can if it reports to the major credit bureaus and you pay on time. But building credit does not mean the card is a good value. Cost still matters.

What should I check before applying?

Check the annual fee, monthly fee, setup or program fee, APR, credit limit, bureau reporting, prequalification language, and whether approval is actually guaranteed. If the terms are hard to understand, pause.

Sources and verification points

This guide uses public consumer-credit guidance and issuer-style disclosure principles. Helpful references include CFPB Regulation Z fee-disclosure rules, CFPB credit card agreement resources, FTC advance-fee scam warnings, and CFPB denial/adverse-action guidance. Card pricing and availability can change, so always verify current terms directly with the issuer before applying.

CFPB fee limitations · CFPB credit card application disclosures · FTC advance-fee warning · CFPB denial guidance