AnyCreditWelcome • Updated May 2026 • Educational credit guide • Estimated read time: 11 minutes

Why Minimum Payments Quietly Cost You Years

Bottom line

Minimum payments keep you from being late, but they are usually the slowest and most expensive way to pay down credit card debt. If you carry a balance, even $25, $50, or $100 extra per month can cut months or years off your payoff timeline.

The real trap is simple: the minimum payment makes this month feel manageable while letting interest drag the debt far into the future.

What is a minimum payment?

A minimum payment is the smallest amount your credit card issuer requires you to pay by the due date to keep the account current. It helps you avoid late-payment damage, but it does not mean your debt is moving fast.

That is why minimum payments feel safe. You see a small number. You pay it. The account stays open. No late fee. No panic.

But if you are carrying a balance, the card issuer is still charging interest. A big part of your payment can go toward interest instead of the actual balance. That is how a $1,500 or $2,500 balance can follow you around for years.

How minimum payments quietly cost you years

Minimum payments cost you years because your payment shrinks as your balance shrinks, while interest keeps adding to the account every month. You feel like you are making progress, but the balance may barely move at first.

Here is the quiet part: the minimum payment is designed to keep the account in good standing. It is not designed to get you out of debt quickly.

That matters even more if you are using a bad-credit, rebuilding, or high-APR card. A high APR can turn small balances into long payoff timelines. You may feel stuck because you are paying every month but not seeing the balance fall fast enough.

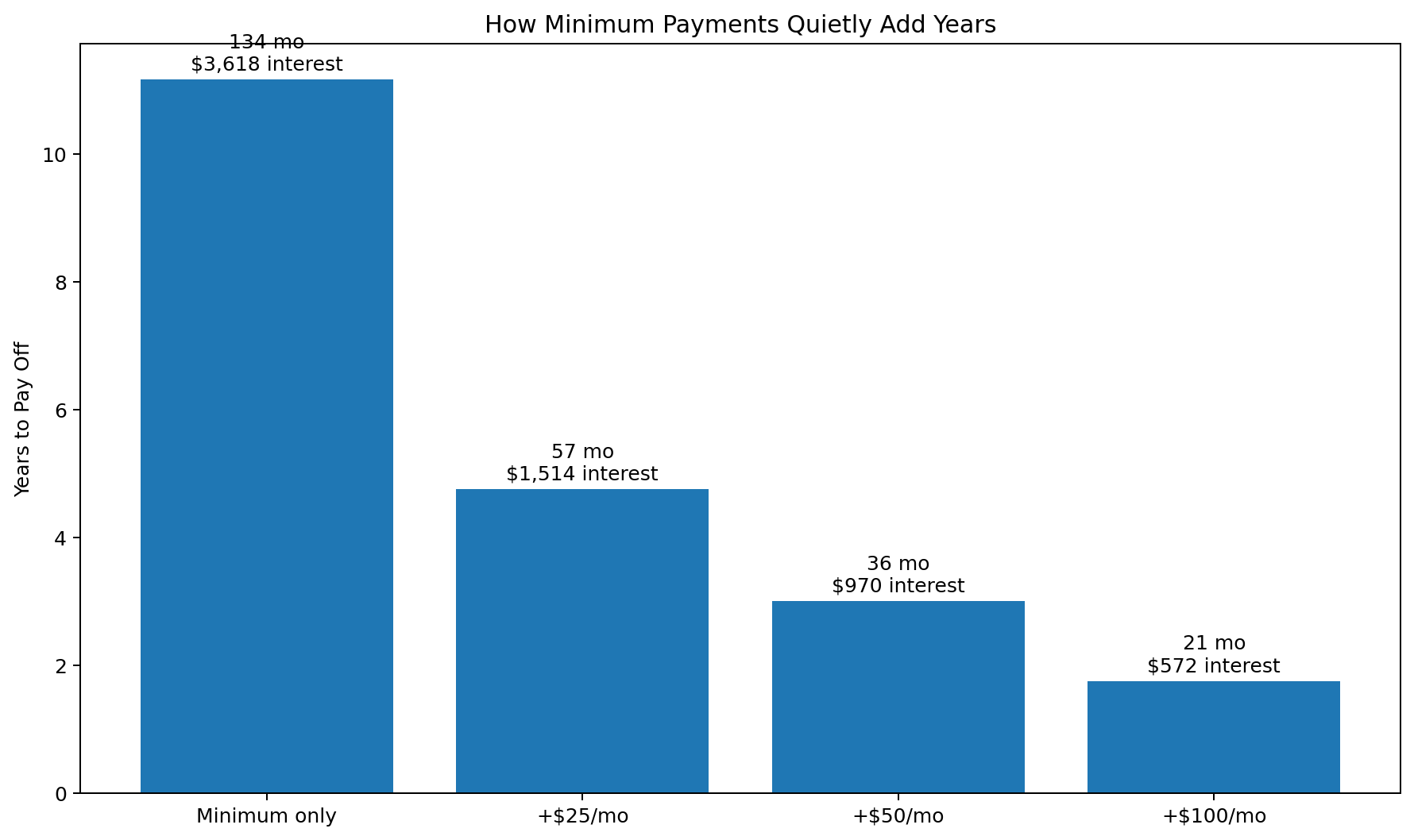

Real example: minimum vs extra payments

On a $2,500 balance at 24.99% APR, paying only the estimated minimum could take about 11 years in this example, while adding $100 per month could cut the payoff to under 2 years. Your exact numbers will depend on your issuer, APR, fees, and minimum-payment formula.

| Monthly strategy | Estimated payoff time | Estimated interest paid | Time saved | Interest saved |

|---|---|---|---|---|

| Minimum only | 11 years 2 months | $3,618 | — | — |

| +$25/mo | 4 years 9 months | $1,514 | 77 months | $2,104 |

| +$50/mo | 3 years | $970 | 98 months | $2,648 |

| +$100/mo | 1 year 9 months | $572 | 113 months | $3,045 |

How minimum payments affect your credit score

Minimum payments can protect your payment history, but they may leave your utilization high for longer. That matters because payment history and amounts owed are the two biggest FICO scoring categories.

Paying at least the minimum on time helps avoid late-payment damage. That part matters a lot. But if the balance stays high compared with your credit limit, your utilization can stay high too.

Utilization means how much of your available credit you are using. If you have a $1,000 limit and a $800 balance, your utilization is 80%. If you pay that balance down to $300, your utilization drops to 30%.

Minimum only

Keeps you current, but may keep utilization high longer. That can make rebuilding feel slow.

Minimum + extra

Lowers the balance faster, which can lower utilization sooner if you do not keep adding charges.

What most people get wrong

The biggest mistake is thinking “I paid the minimum” means “I am making real progress.” Sometimes it does. Often it only means you avoided being late.

Mistake #1: Paying extra once, then stopping

One extra payment helps. A repeatable extra payment helps more. Consistency beats one dramatic month.

Mistake #2: Adding new charges

If you pay $50 extra but add $200 in new charges, the balance still moves the wrong way.

Mistake #3: Ignoring APR

High APR balances punish slow payoff. That is why bad-credit cards need extra care.

Mistake #4: Waiting for a perfect plan

You do not need a perfect strategy. You need a small extra payment you can repeat.

A simple plan that actually works

The safest plan is to pay the minimum automatically, then add one fixed extra payment you can afford every month. Start small. Make it boring. Let the repeated action do the work.

Protect your payment history first. Late payments can hurt more than a small balance.

Choose $25, $50, or $100. The best number is the one you can repeat without creating new debt.

Do not wait until the end of the month when money is already gone.

If you must use the card, keep new spending smaller than your extra payment.

Your score may move slowly, but lower balances are still progress.

Minimum payment vs extra payment

The minimum payment is better for staying current, while an extra payment is better for getting free from the balance. Most people need both: the minimum to protect the account, and the extra payment to make the debt shrink faster.

| Option | Best for | Strength | Weakness |

|---|---|---|---|

| Minimum only | Preventing late payments | Keeps the account current | Can stretch payoff for years |

| Minimum + $25 | Starting small | Easy first step | Still takes patience |

| Minimum + $50 | Faster balance reduction | Can save meaningful time and interest | Requires monthly discipline |

| Minimum + $100 | Aggressive payoff | Moves the balance much faster | May not fit every budget |

Who this is best for

This strategy is best for people who are carrying a balance but still have enough cash flow to pay a little more than the required minimum. It is especially useful if you are trying to rebuild credit and want to lower utilization.

- Bad-credit card users who want to avoid staying stuck with a high balance.

- Fair-credit rebuilders who want utilization to fall before applying for better cards.

- People with high APR cards who need to reduce interest pressure.

- Anyone paying on time but feeling like the balance never moves.

When paying extra may not be the first move

Paying extra is powerful, but it may not be your first move if you are behind on essentials or missing minimum payments on other accounts. Protect the basics before attacking one balance harder.

Bottom-line decision

If you only pay the minimum, you may stay current but stay stuck. If you pay even a small amount extra every month, you can cut interest, lower balances faster, and give your credit a better chance to recover.

Common questions

Is paying the minimum bad?

No. Paying the minimum is much better than paying late. The problem is using the minimum as your full payoff plan when you can afford more.

Will paying extra raise my credit score?

It can help if it lowers your credit utilization, but no score increase is guaranteed. Your score also depends on payment history, account age, credit mix, new credit, and other profile details.

Is it better to pay once or multiple times per month?

Either can work. Multiple payments may help you keep the balance lower during the month, but the most important move is paying on time and reducing the balance.

Should I pay extra on the highest APR card first?

Usually yes, if your goal is to save the most money. If your goal is quick motivation, paying down the smallest balance first can also help. The best plan is the one you will actually follow.

What if I cannot afford extra payments right now?

Pay the minimum on time and avoid new charges where possible. Even stabilizing the balance is progress. When your budget opens up, start with a small extra amount.

Sources and notes: This article is educational and not financial advice. Credit card terms and minimum payment formulas vary by issuer. The payoff math above is an example only.

Reference materials include CFPB guidance explaining that paying more each month reduces interest over time, FICO education on payment history and amounts owed, CFPB Regulation Z repayment disclosure materials, and Federal Reserve consumer materials on minimum payment warnings.

CFPB: paying more than the minimum • FICO score factors • CFPB repayment disclosure appendix • Federal Reserve minimum payment warning example