See the month your credit card debt hits zero.

Enter your cards once. See your real debt-free date and how much sooner an extra $25 or $50 a month ends it.

No credit check · no log-ins · no card numbers · nothing leaves your browser

Total debt

$18,400

Debt-free by

Nov 2028

How “Nov 2028” is found: each month we apply APR ÷ 12 to your balance, subtract your payment, and roll the rest. The first month your balance crosses $0 is your debt-free month.

Exact debt-free date

Not a vague range—the specific month your last card hits $0.

Snowball vs. avalanche

See both strategies side-by-side and pick what fits you.

Nothing leaves your browser

No accounts, no card numbers, no data saved on our servers.

How it works

No logins. No credit pulls. No spreadsheet skills. Just three short steps to a real debt-free date.

- 1~20 sec

Add what you owe

Enter each balance, APR, and minimum payment. Most people do this from the back of one statement.

BalanceAPR %Min payment - 2~10 sec

Pick your strategy

Snowball for momentum, avalanche for max interest savings, or set a target debt-free date and we'll back into the math.

SnowballAvalancheTarget date - 3Instant

See your payoff plan

Your exact debt-free month, total interest, and the monthly amount that gets you there. Print it, save it, share it.

Debt-free dateInterest savedMonthly target

What an extra $25 or $50 a month actually does

Same card. Same APR. Three different futures. Example: a $5,000 balance at 22.99% APR with a typical 3% minimum payment.

Minimum only

+$0/mo18 yrs 2 mo

to debt-free

Interest paid: $7,870

Most of every payment goes straight to interest.

Minimum + $25

+$25/mo8 yrs 2 mo

to debt-free

Interest paid: $4,120

Cuts roughly 10 years and ~$3,750 in interest.

Minimum + $50

+$50/mo5 yrs 5 mo

to debt-free

Interest paid: $2,870

Saves about 13 years and ~$5,000 in interest.

Illustrative example using standard amortization (interest = APR ÷ 12 × balance, posted monthly). Your card’s exact minimum rule and any fees can shift the timeline by weeks. Run your own balances below for your real numbers.

Who this payoff planner is built for

Yes, it’s for you if…

- You’re juggling more than one credit card or loan.

- You’re tired of only seeing the minimum payment and not the end date.

- You want a simple plan you can change as life changes.

Not a fit if…

- ×You’re looking for investment advice or stock picks.

- ×You want us to pull your credit report (we don’t).

- ×You’re hoping for a magic button that fixes everything overnight.

Common questions

Plan payoff for your credit cards

Pick the calculator that fits your situation — see all tools on the Tools page.

Loan, mortgage, paycheck, and percentage calculators live on the Tools page.

From the blog

Smart, no-shame reads on getting out of debt

Best Business Credit Cards 2026: Stop Burning Rewards on Your Personal Card

Compare 2026's biggest sign-up bonuses, real point valuations, the 5-Filter Business Card Test, and the 90-Day Setup Plan to earn $1,500–$6,000 in rewards.

Best Credit Builders for 2026: Stop Guessing Which One Fits

Compare SuperMoney, Grow Credit, WalletHub Credit Builder, and Sezzle Up by situation, costs, credit reporting, trial terms, risks, and the best first step before applying.

Read the review

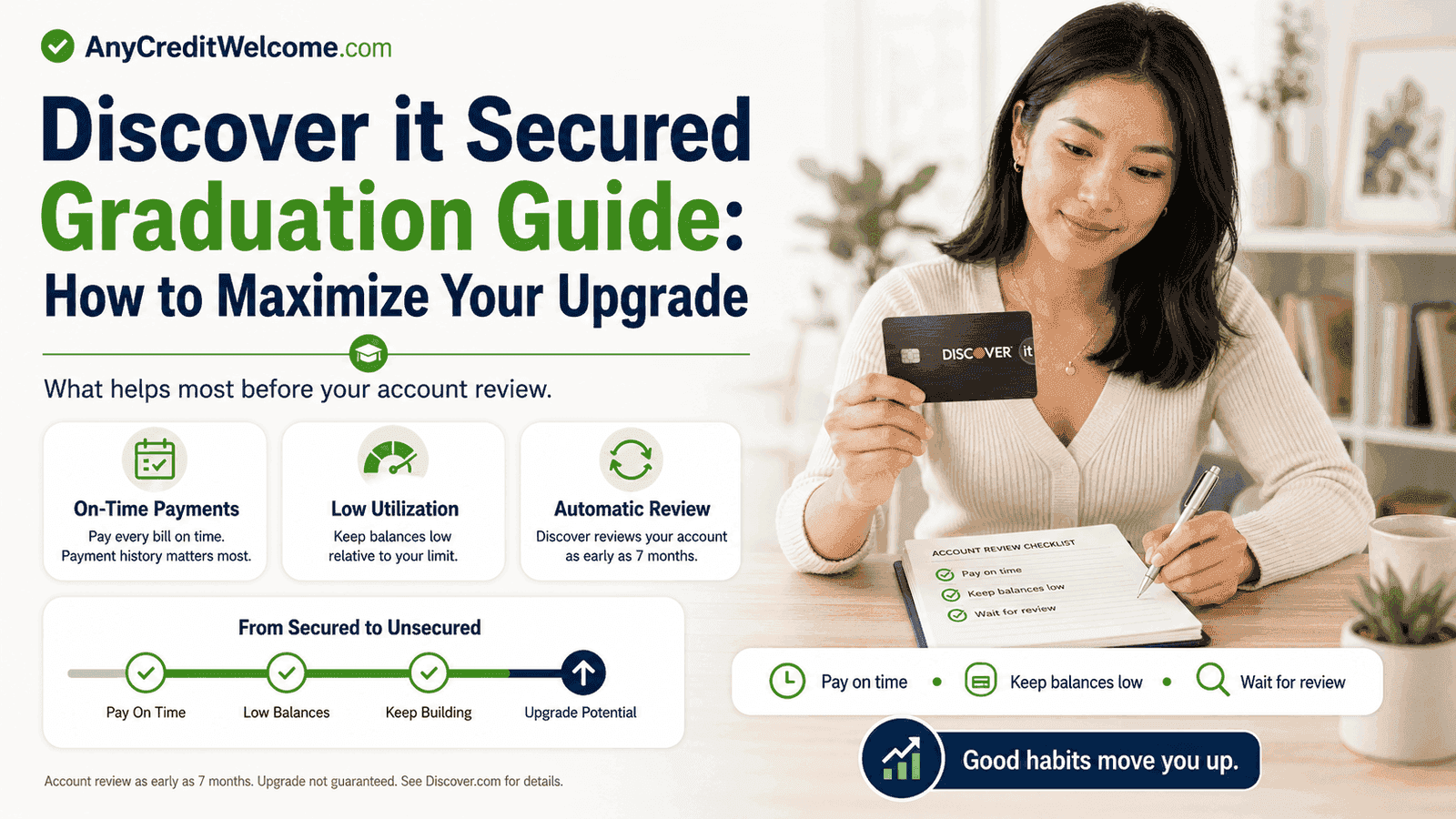

Discover it Secured Graduation Guide: How to Maximize Your Upgrade

How graduation works, how to maximize your upgrade, protect your deposit, manage utilization, and avoid mistakes before review.

11 min read

Credit Utilization Explained — and How to Time Payments

The single biggest lever on your credit score, plus how to time a payment so it actually helps.

5 min read

Average American Credit Card Debt in 2026

Total balances, average debt per person, debt by generation, APR pressure, and what to do next if you're carrying a balance.

10 min read

Fee Trap Credit Cards: How to Spot Bad-Credit Card Fees Before You Apply

Annual fees, monthly fees, setup fees, authorized-user fees — how to spot them in a card offer before you apply.

9 min read

Your payoff checklist

Knock these out before (or while) you build your plan.

- 1Gather every debt: balance, interest rate, and minimum payment.

- 2Note your monthly take-home income and essential bills.

- 3Decide a realistic extra amount you can put toward debt each month.

- 4Pick a payoff method (snowball for motivation, avalanche for savings).

- 5Set a target debt-free date and add it to your calendar.

- 6Schedule a 10-minute monthly check-in to update your numbers.

Disclaimer

AnyCreditWelcome provides educational tools and estimates only. We are not a lender, financial advisor, credit counselor, or law firm. Calculations are based on the information you enter and standard interest formulas; your actual payoff timeline, fees, and minimum payments may vary based on your lender’s terms. Nothing on this site is financial, legal, or tax advice. Please consult a qualified professional before making major financial decisions.